Think about the last time you avoided checking your bank account. Or the last time you got a raise but somehow still felt financially anxious. Or the moment you were on the verge of a smart investment — and then talked yourself out of it with an excuse that, looking back, didn't quite make sense.

Those moments aren't random. They're patterned. And the pattern usually traces back not to your current financial situation, but to what you learned — or absorbed — about money when you were very young.

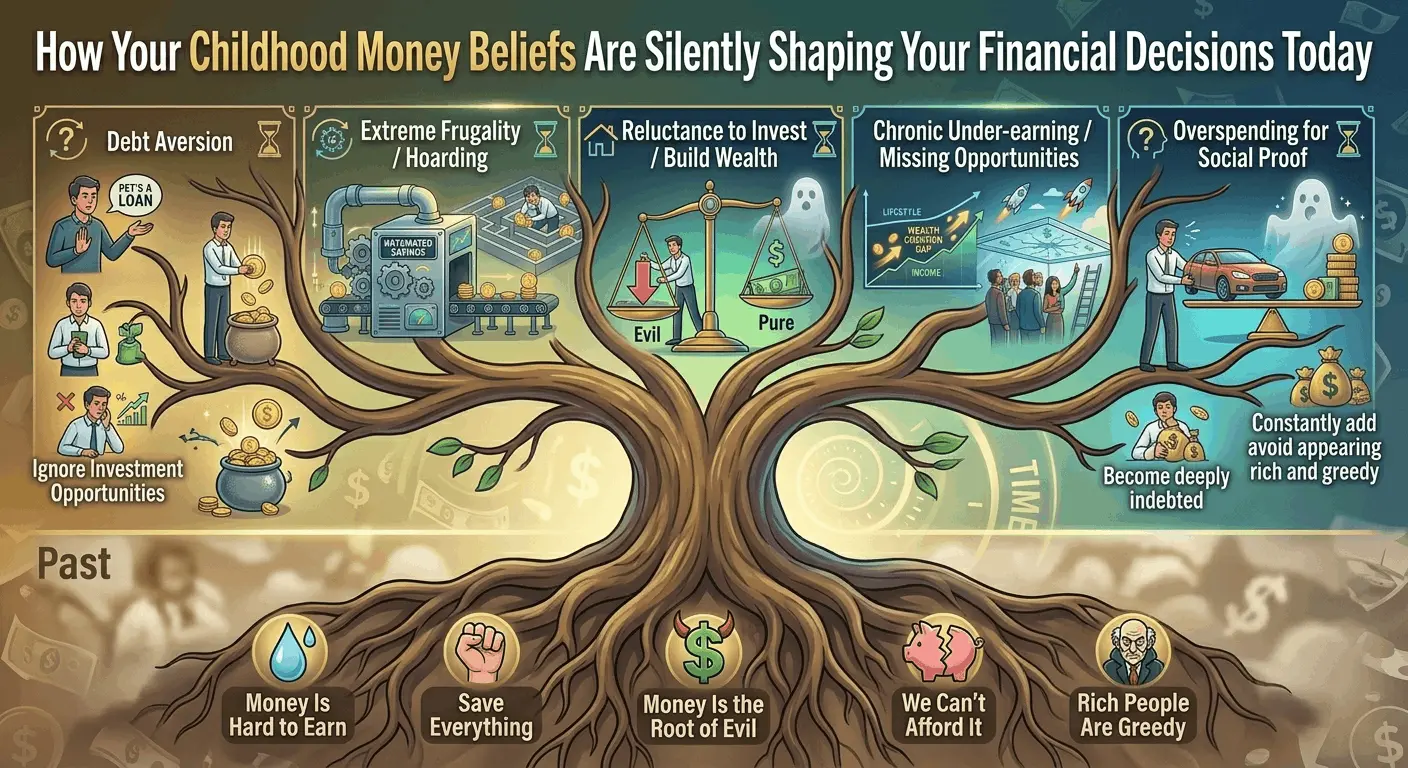

How Money Beliefs Actually Form

Children don't learn about money primarily through formal education. They learn it through observation and emotional context. What they see their parents do with money. The tension in their household when bills arrived. Whether financial conversations were calm or secretive or charged with anxiety. Whether wealth was talked about with admiration or suspicion.

By around age 7, most children have already formed foundational beliefs about money — whether it's scarce or abundant, whether rich people are admirable or greedy, whether financial success is achievable for "people like us" or reserved for someone else.

The most persistent financial beliefs aren't the ones we consciously chose — they're the ones we absorbed without realizing it, in environments where we had no defenses against them.

These beliefs become invisible precisely because they feel like facts. You don't notice the belief that "there's never enough money" — you just notice that you feel anxious whenever your account drops below a certain threshold, regardless of how much money is actually there. The belief is the operating system; your financial behavior is just the program running on top of it.

The 7 Most Common Financial Limiting Beliefs

Not all limiting money beliefs are equal. Some are surface-level — easy to spot and relatively easy to reframe. Others are deeply structural and can take consistent work to shift. Here are the seven patterns that appear most frequently:

1. "Money is the root of all evil"

Often absorbed from religious or cultural environments. People who hold this belief unconsciously resist accumulating wealth because, at some level, they associate it with moral corruption. They may find themselves generously spending or giving away money just as their balance grows. The financial sabotage is the belief protecting their self-image.

2. "Rich people are greedy / untrustworthy"

A variation of the above. If wealth is coded as a character flaw, someone with this belief will unconsciously avoid becoming wealthy to avoid becoming that kind of person. They may champion financial underdog status as a badge of character.

3. "I don't deserve abundance"

This one often shows up in people who had difficult childhoods or absorbed messages about their worth being conditional. When money does arrive, it feels uncomfortable — like wearing someone else's clothes. The solution often involves self-sabotage to get back to a "deserved" level.

4. "Talking about money is rude/taboo"

People raised in households where money was a forbidden topic often struggle to negotiate salaries, discuss pricing, or even articulate their own financial goals out loud. The silence itself becomes an obstacle to financial literacy.

5. "You have to work extremely hard to earn money"

This one seems positive — and it has some truth to it — but taken too far, it creates resistance to passive income, investment returns, and systems that generate money without direct labor. People with this belief often feel vaguely guilty about money they didn't "earn" through suffering.

6. "More money = more problems"

Usually absorbed from cultural messaging or from watching someone close to them struggle with increased financial complexity. This belief makes wealth feel threatening rather than enabling.

7. "We're just not a wealthy family"

Perhaps the most quietly powerful of all. It frames financial limitation as a fixed identity rather than a temporary circumstance — and identity-level beliefs are the hardest to change because they feel like truth rather than opinion.

🔍 Quick Self-Assessment

Ask yourself these questions honestly — your gut reaction (not your intellectual answer) is the data:

- When I imagine myself being significantly wealthier, what's my first emotional reaction?

- Do I find myself quietly judging wealthy people? What specifically?

- When I get unexpected money (bonus, gift, windfall), what do I do with it immediately?

- Do I feel more comfortable talking about my problems than my financial wins?

- Has my income grown but my net worth hasn't followed?

Why These Beliefs Are So Hard to Override With Information

Here's the frustrating reality: you can know exactly what you're supposed to do financially — max your 401(k), diversify, build an emergency fund, invest early — and still not do it. Or do it for a while and then quietly stop.

That's not laziness. That's a deeply wired belief system winning an invisible argument against your conscious intentions. Information operates at the level of logic. Beliefs operate at the level of identity and emotion. Logic rarely wins that fight directly.

This is why so many personal finance books fail to produce lasting change. They deliver information — which is genuinely useful — but they can't address the emotional infrastructure that's filtering every financial decision you make.

What Actually Changes Financial Beliefs

Three things have genuine evidence behind them for shifting deeply held financial beliefs:

1. Making the belief explicit

You can't examine what you can't name. The first step is identifying the specific belief — not a vague "I'm bad with money" but something precise: "I believe that people who accumulate wealth are self-serving, and I don't want to be that." Once it's explicit, you can interrogate it.

2. Tracing it to its origin

Where did this belief come from? When you trace it back to a specific memory, person, or environment, it often loses some of its authority. A belief installed by a financially stressed parent doing their best doesn't have to govern your decisions as a 40-year-old with completely different circumstances.

3. Building contradictory evidence over time

Beliefs change most durably when your real-world experience contradicts them repeatedly. Small financial wins, sustained over time, gradually rewrite the operating system. This is why mindset work needs to be paired with actual financial behavior — not just reflection.

The goal isn't to become someone who doesn't think about money emotionally — that's impossible. The goal is to become someone whose emotional relationship with money serves them rather than limits them.

How TPP System Approaches This Problem

The True Prosperity Path (TPP System) is built around exactly this challenge. The opening modules focus not on investment tactics but on mapping and disrupting the belief systems that block financial growth — before introducing strategies that require those beliefs to be functional.

That sequencing matters. Teaching asset allocation to someone who unconsciously believes they don't deserve wealth is like giving them a map while they're still convinced they're not allowed to travel. The map becomes useless.

TPP's approach — mindset work first, strategy second — is one of the things that distinguishes it from standard financial education. Whether it works for you depends on how willing you are to do the inner work that the first modules require. But for people who've consumed financial content without changing their behavior, this kind of root-cause approach is often what's actually been missing.

Ready to Examine Your Own Financial Blueprint?

TPP System walks you through identifying and rewriting the beliefs that might be your real financial ceiling — alongside proven wealth-building frameworks. 60-day money-back guarantee.

Explore TPP System →A Practical Starting Point

You don't need a full program to start identifying your financial beliefs. Here's a simple exercise you can do right now:

- Finish this sentence in writing (not in your head): "People who have a lot of money are ___________." Write the first 5 things that come to mind without filtering.

- Look at what you wrote. Is it mostly positive? Mostly negative? Mixed? Each word is a data point about your subconscious financial relationship.

- Ask: where did I learn this? Often, you can trace it directly — a parent's comment, a cultural message, a specific experience that got generalized into a rule.

- Ask: is this actually true? Not "is it sometimes true" but: "is this a useful, accurate framework for how I want to engage with money?" If not, what would a more useful belief be?

This sounds simple. It is, technically. But most people have never done it in writing, which is where it actually works. The page externalizes the belief so you can see it rather than just feel it.

The Bottom Line

Your financial outcomes are downstream of your financial beliefs. That doesn't mean mindset is everything — circumstance, timing, access, and knowledge all matter enormously. But when two people with similar access to opportunity consistently get different results, the difference usually lives in their internal frameworks, not their external resources.

Identifying your limiting beliefs isn't a spiritual exercise. It's a practical one. And it's often the missing piece in financial education that focuses only on tactics.