There's no shortage of financial education available. Books, podcasts, YouTube channels, courses — the information supply is effectively infinite. And yet, the gap between people who understand financial concepts and people who actually build wealth remains stubbornly wide.

This isn't an information problem. Most people who struggle financially could pass a quiz on compound interest, index fund diversification, and the importance of saving early. The knowledge is there. What's missing is a different layer — the principles that govern how people actually apply financial knowledge over time.

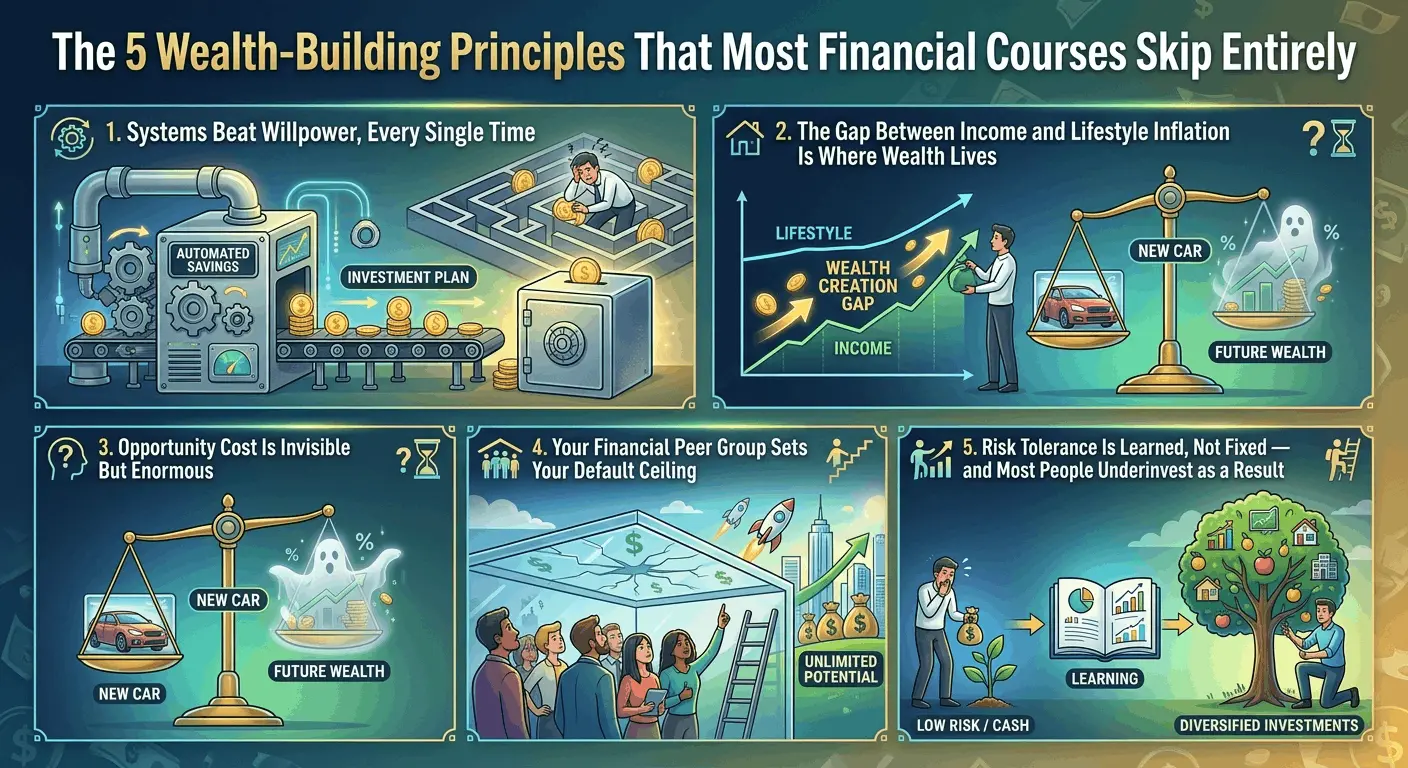

Here are five of them that most financial education skips — not because they're secret, but because they're harder to package into a simple rule or a numbers-based framework.

Systems Beat Willpower, Every Single Time

Most personal finance advice is implicitly willpower-based: spend less, save more, don't buy the latte. This works for about three weeks. Willpower is a depletable resource. Financial discipline based on willpower eventually fails — and when it fails, it often fails catastrophically (a spending binge that undoes months of restraint).

Lasting wealth builders do something different: they make financial decisions once and then automate them. Automatic contributions to retirement accounts. Automatic transfers to savings on payday. Bill automation that removes the decision entirely. The goal is to design the environment so that the right financial behavior happens by default — not by discipline.

The practical implication: Before adding another "I should be better about money" rule to your internal monologue, ask: what can I automate so I never have to make this decision again?

The Gap Between Income and Lifestyle Inflation Is Where Wealth Lives

Most people experience this: income increases, and within a year, so does spending. The raise gets absorbed by a nicer car, a bigger apartment, more frequent dining out. This is lifestyle inflation — and it's almost universal.

The people who build wealth over time are not necessarily the highest earners. They're the people who consistently allow the gap between their income and their spending to grow — and redirect that gap into assets. The actual math is straightforward. The behavioral challenge is enormous.

This is why the people who retire comfortably on $80,000/year incomes often have more wealth than people who earned $200,000/year for 20 years. Income creates the potential. Lifestyle management determines whether that potential converts to wealth or evaporates.

The practical question: When your income grows next, what percentage of the increase will you redirect to assets before lifestyle costs can absorb it?

Opportunity Cost Is Invisible But Enormous

Every financial decision involves not just what you're spending or saving, but what you're forgoing. The real cost of spending $10,000 isn't $10,000 — it's what that $10,000 would have become over 20 years invested in a diversified portfolio. The real cost of sitting in cash for 5 years "waiting for the right time to invest" isn't zero — it's the compounded growth that didn't happen.

Most financial education teaches you to evaluate purchases in isolation: "Can I afford this?" Wealth builders evaluate purchases in context: "What is the real cost of this decision, including what I'm giving up?"

This isn't about never spending money on things you enjoy. It's about making those decisions with full visibility into what they actually cost — so you can make them intentionally rather than by default.

Your Financial Peer Group Sets Your Default Ceiling

This one is uncomfortable to acknowledge because it suggests that who you spend time with significantly influences your financial outcomes. But the evidence — both anecdotal and research-based — is compelling: people tend to calibrate their spending, saving, investment activity, and financial ambition to what's normal in their immediate social environment.

If everyone in your peer group spends freely and never discusses investment or savings, that becomes the default. If you're surrounded by people who treat wealth-building as a normal adult activity — who discuss asset allocation, who celebrate net worth milestones, who share investment strategies — your baseline shifts.

This doesn't mean abandoning your current relationships. It means deliberately seeking additional exposure to the financial behaviors you want to normalize. Mastermind groups, investment clubs, financial communities — the community element of programs like TPP System exists for exactly this reason.

The honest audit: In your current social environment, is ambitious wealth-building normal or slightly embarrassing? That framing is doing more to your financial outcomes than you probably realize.

Risk Tolerance Is Learned, Not Fixed — and Most People Underinvest as a Result

Many people treat their risk tolerance as a personality trait — "I'm just not a risk-taker." But risk tolerance is largely a function of financial education, past experience, and emotional conditioning. And because most people have had very little financial education and often strong negative emotional experiences with money, they tend to default to conservative behavior that systematically underperforms over long time horizons.

Keeping excess cash in a low-yield savings account "because it's safe" is a form of risk — inflation risk, opportunity risk. It feels safe because you're not watching a number fluctuate. But over a 20-year period, the risk of sitting in cash can dramatically exceed the risk of a diversified investment portfolio.

Understanding this intellectually is step one. Building genuine comfort with appropriate risk — through education, exposure, and small early experiences with investing — is the work that actually shifts behavior.

The most effective wealth-building strategy isn't the one with the highest projected return. It's the one you'll actually stick with for 20 years without making fear-based decisions in the middle.

Why These Principles Matter More Than Tactics

If you have the five principles above working in your favor, almost any reasonable financial tactic will work. If you don't have them, even a technically optimal strategy will fail — because you'll abandon it, circumvent it, or choose not to start it at all.

This is the central argument behind programs that focus on financial mindset before financial tactics. The TPP System (True Prosperity Path) is built on exactly this premise — addressing the psychological and behavioral infrastructure first, then layering in strategy education once the foundation can actually support it.

📋 The 5 Principles — Summary

- 01: Systems beat willpower — automate your financial defaults

- 02: Protect the gap between income and lifestyle — redirect growth into assets

- 03: Make opportunity cost visible in every financial decision

- 04: Audit your financial peer group — it's setting your behavioral ceiling

- 05: Treat risk tolerance as something you build, not something you're born with

Where to Start if You're Building From Scratch

If reading this has surfaced some honest gaps in your own financial behavior — don't let that become discouraging. These are patterns, not personality traits. They can be changed. But changing them requires more than information. It requires the kind of consistent, structured engagement that forces you to examine your own behavior and gradually build new defaults.

The most effective starting point is usually the simplest one: pick one of the five principles above — the one where you recognize yourself most clearly — and spend the next 30 days designing your behavior around it. Not trying harder. Designing differently.

Automate one savings transfer you currently do manually. Calculate the real 20-year cost of one purchase you're considering. Find one person in your life who takes wealth-building seriously and have a genuine financial conversation with them. Start somewhere specific and observable — not with a general intention to "be better with money."

Want a Structured Framework for All Five?

TPP System walks you through applying each of these principles with curriculum-based modules, real exercises, and a community that holds you accountable. Protected by a 60-day guarantee.

See What's Inside TPP System →The Bottom Line

Most financial courses teach you what to do. The gap between that knowledge and actually doing it — consistently, over years, through market cycles and life changes and the constant pull of lifestyle inflation — lives in the five principles above.

They're not glamorous. They don't promise a specific return. But they're the actual mechanism through which lasting wealth is built, and they're what most financial education quietly skips because they're harder to teach than a compound interest formula.